Why Compare CU80 Car Insurance?

Specialist Support for CU80 Convictions

Clean Green Cars introduces you to specialist brokers experienced with CU80 mobile phone offences. With 6 penalty points on your licence, many standard insurers may decline to quote, but specialist brokers could still offer cover.

Six Points Does Not Mean One Price

A CU80 conviction for using a mobile phone while driving carries a significant point penalty, yet the premium loading could differ substantially between insurers. Comparing quotes may help you find a more competitively priced policy.

One Simple Form to Get Started

Instead of explaining your CU80 conviction repeatedly to different brokers, Clean Green Cars lets you fill in one form and receive quotes from several specialists with no obligation to buy.

CU80 Car Insurance At A Glance

- Mobile Phone Conviction – CU80 means using a handheld mobile phone while driving under Section 41D of the Road Traffic Act 1988.

- 6 Points, Not 3 – CU80 carries double the points of most other construction and use codes, staying on your licence for 4 years from the date of offence.

- The Most Common CU Code – because CU80 is so widespread, most insurers have established pricing processes and specialist brokers see it every day.

- Start comparing CU80 quotes through specialist brokers using the form above.

What Is a CU80 Conviction?

CU80 is a statutory offence under Section 41D of the Road Traffic Act 1988 – breach of requirements as to control of the vehicle, which in practice almost always means using a handheld mobile phone while driving. Here’s how the law defines it:

- Who it applies to – Any driver of a motor vehicle on a road who does not have proper control. Since March 2022 the rules specifically cover handheld device use in almost any situation while the engine is running, including when stopped in traffic or at lights.

- What counts as loss of control or handheld use – Making or receiving calls, texting, scrolling social media, taking photos or videos, selecting music, or any interactive use of a handheld phone or device. It also covers being positioned in a way that prevents full control of the vehicle.

- How the duty arises – Automatically, the moment you drive on a public road. Hands-free use remains legal if the phone is securely mounted, but you can still be prosecuted under CU80 if a hands-free call is judged to have caused you to lose proper control.

| Penalty | Details |

|---|---|

| Penalty Points | A CU80 carries 6 penalty points (doubled from 3 in March 2017). New drivers lose their licence at 6 points. |

| Duration on Licence | 4 years from the date of the offence. Most insurers ask about convictions from the last 5 years. |

| Fixed Penalty | £200 and 6 points (up from £100 and 3 points before March 2017). |

| Maximum Court Fine | £1,000 for private vehicles. £2,500 for PCV and goods vehicle drivers. |

| Driving Ban | Discretionary. New drivers within first 2 years face automatic licence revocation. |

| Legislation | Section 41D, Road Traffic Act 1988 |

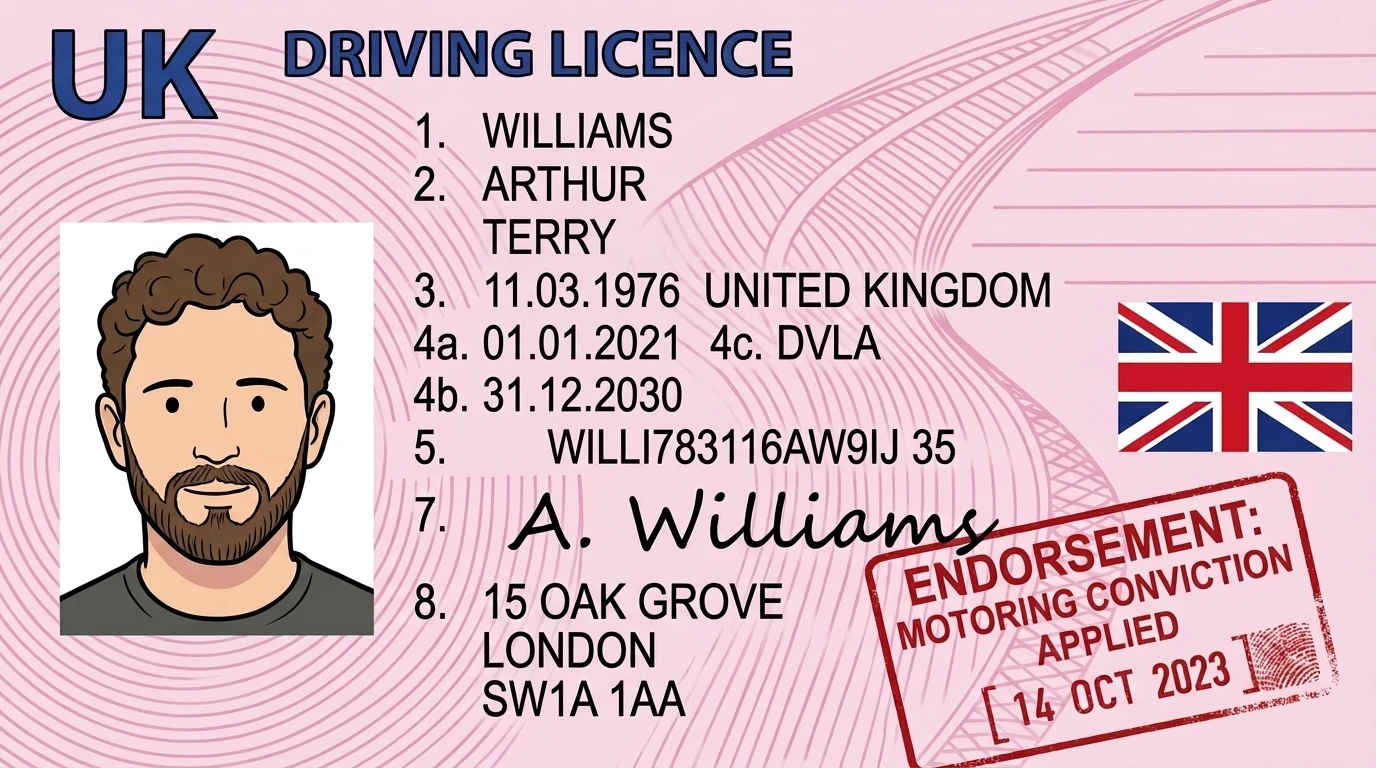

CU80

CU80Can You Get Insurance With a CU80?

Yes, but the market is narrower than for a standard policy, and you’ll almost always need a specialist broker. Here’s what to know before you compare:

- Points and ban – 6 penalty points and a fixed penalty of £200 (doubled in March 2017), with a discretionary court ban. New drivers within their first 2 years face automatic licence revocation at 6 points.

- Time on your record – 4 years on the DVLA endorsement, and most insurers ask about convictions in the last 5 years.

- When it’s spent – A fine-only CU80 is spent 1 year after conviction under the Rehabilitation of Offenders Act 1974.

- Disclosure always matters – Non-disclosure can invalidate the policy and lead to a claim being declined. CU80 carries more weight than a typical 3-point construction and use code because the 6 points signal a behavioural lapse.

- Treated as a behavioural offence – Because CU80 is so widespread, most insurers will still quote, but you can expect a larger loading than for purely mechanical codes. Specialist brokers tend to find the most proportionate prices.

Clean Green Cars introduces you to specialist brokers experienced with Construction and Use convictions. If you need short-term cover while comparing, temporary car insurance with convictions may bridge the gap.

Who Needs CU80 Car Insurance?

CU80 is the most common construction and use code. It affects drivers from all backgrounds and experience levels. Here is who typically needs to compare CU80 car insurance quotes.

Glanced At A Sat Nav Notification

The screen flashed a route change or traffic alert. You looked down for a second — not even long enough to read it — and a camera or officer caught the moment. It feels absurd that a glance carries 6 points.

Picked Up A Ringing Phone On Reflex

The phone rang and your hand reached for it without thinking. Years of habit overrode a rule you know perfectly well. The reflex lasted a second but the points last four years.

Held Phone At Traffic Lights — Still Counts

The car was stationary, the engine was running, and you checked a message thinking it was safe. The law makes no distinction between moving and stopped in traffic. It still counts as CU80.

New Driver — Single Offence Means Licence Gone

Six points within your first two years and your licence is revoked automatically. One mistake, and you are back to learner status, retaking both tests, paying for lessons again. Your independence vanished overnight.

Delivery Driver Checking The App

The job requires you to follow an app for routes and drop-offs. You checked it while driving because stopping for every notification would make the job impossible. Now your livelihood is at risk over the tool you need to do the work.

Worth Knowing: CU80 is one of the most common conviction codes in the UK. Clean Green Cars connects you with brokers who handle these cases every day and understand that one moment does not define your driving record.

What CU80 Car Insurance Covers

A CU80 on your licence does not change what your policy is designed to cover. It changes how much you pay and which terms your insurer may apply. Because CU80 is so common, most insurers can still offer all three cover levels.

Here is what each level of cover could include. Please note that policy features, benefits, terms and conditions vary among insurers, so always check the policy wording.

| Feature | Comprehensive | Third Party, Fire & Theft | Third Party Only |

|---|---|---|---|

| Damage to your own vehicle | Yes | No | No |

| Fire and theft protection | Yes | Yes | No |

| Damage to other people's property | Yes | Yes | Yes |

| Injury to other people | Yes | Yes | Yes |

| Windscreen cover | Often included | Rarely | No |

| Courtesy car | Sometimes included | Rarely | No |

| Personal belongings | Sometimes included | No | No |

Cover Tip: A brief glance at a notification in stationary traffic and deliberately texting at 70mph both produce the same CU80 code. Specialist brokers understand the range of circumstances behind this conviction and could help you find an insurer who prices your specific situation fairly.

What CU80 Car Insurance May Not Cover

A single missed detail could mean a claim gets declined. Drivers with a 6-point CU80 should pay close attention. Here is what is typically excluded.

Standard Exclusions

- Undeclared Convictions - If you do not tell your insurer about your CU80 or any other convictions, they could invalidate your policy and may decline all claims.

- Driving Under the Influence - If you cause an accident while impaired by drink or drugs, your insurer could decline your claim regardless of any other conviction on your record.

- Undeclared Vehicle Modifications - If your vehicle has been modified and you have not told your insurer, they could treat a claim differently or decline it.

- Using Your Car for Undeclared Purposes - If you use your car for business or hire without declaring it, your insurer may not cover a claim.

- Phone Use at Time of Accident - If you cause an accident while using your phone - even after a CU80 conviction - your insurer could decline or reduce a claim. Phone records may be checked.

- Unlicensed Drivers - If someone without a valid licence drives your car and causes damage, your insurer may decline the claim.

- New Driver Licence Revocation - If your licence was revoked under the New Drivers Act and you drive before repassing your test, any insurance claim could be declined.

- Wear and Tear - General wear and tear, mechanical breakdowns, and gradual deterioration are typically not covered under motor insurance policies.

Optional Extras Worth Adding

Your standard policy is designed to cover the basics. These extras fill the gaps that could matter most after a mobile phone conviction.

A black box tracks your driving to help demonstrate safe habits after a CU80. May help reduce your premium at renewal.

May help cover roadside assistance if your car breaks down, subject to policy limits and conditions.

May help cover your legal costs if you need to dispute fault after an accident, depending on your policy terms.

May help you recover losses from a non-fault crash, subject to policy limits and conditions.

May pay a set amount if you are hurt in a crash and cannot work, depending on your policy terms.

May help cover the cost of replacing your keys if they are lost or stolen, subject to policy limits and conditions.

What Affects the Cost of Car Insurance With a CU80 Conviction?

Your quote depends on your driving record, your vehicle, and whether the CU80 sits alongside other endorsements. The 6-point penalty means CU80 carries more weight with insurers than a typical 3-point construction and use code.

Here are the key factors that could affect your price.

| Key Factor | Impact on Your Price |

|---|---|

| Your CU80 conviction | CU80 carries 6 points - double most other CU codes. This is a significant loading factor for insurers. |

| New driver status | New drivers who lost their licence under the New Drivers Act and repassed their test may face higher premiums than experienced drivers with CU80. |

| Time since offence | Your price could drop each year as the CU80 ages. A conviction from several years ago may cost less to insure than a recent one. |

| Other convictions on your licence | A CU80 on top of other motoring convictions may increase your premium further. Six points already takes you halfway to the totting-up threshold. |

| Your vehicle | Higher insurance group cars cost more to insure. A lower-group vehicle could help offset the CU80 loading. |

| Your age and experience | Younger or less experienced drivers may face higher premiums, especially with 6 points on their record. |

| Where you live | Your postcode affects your premium. Areas with higher claim rates typically cost more to insure. |

| Annual mileage | Lower mileage could mean a lower premium. Only declare what you expect to drive. |

Price Insight: CU80 carries 6 points, double most other construction and use codes. That said, because it is the most common CU conviction, specialist brokers have extensive experience placing these cases. Your loading could reduce noticeably with each clean year.

Ways to Cut Your Car Insurance Cost

A CU80 could push your premium up noticeably because of the 6-point penalty. Here are practical steps that could help.

Compare at Every Renewal

Do not auto-renew. Your CU80 loading could reduce each year. Get quotes above to check what is available now.

Consider a Telematics Policy

A black box gives your insurer hard evidence that your CU80 was a one-off. Consistent safe driving data could help bring your renewal down.

Put Your Phone Out of Reach

A glove box, a bag on the back seat - if your phone is not within arm's reach, the temptation disappears. It also prevents a second CU80, which would be much harder to insure.

Choose a Lower Insurance Group Car

Cars in lower groups cost less to insure. If you are changing vehicles, checking the group first could help offset the 6-point loading from your CU80.

Increase Your Voluntary Excess

A higher excess could lower your premium. Only offer what you could genuinely afford if you needed to claim.

Build a Clean Record

Every conviction-free year after your CU80 shows insurers it was a momentary lapse, not a pattern. Clean years are your strongest bargaining tool at renewal.

Reduce Your Annual Mileage

Lower mileage means lower risk. If you can cut your declared mileage, it could help offset some of the CU80 loading.

Saving Tip: Everyone knows they should not pick up their phone while driving. But habits are hard to break, and a single moment of distraction does not make you an unsafe driver in every other respect. Compare quotes above to find brokers who price the full picture, not just the points.

How to Compare CU80 Car Insurance Quotes

Getting quotes after a CU80 does not take long. Clean Green Cars connects you with brokers who cover convicted drivers every day. Get started above when you are ready.

Enter Your Vehicle Details

Add your registration, make, model, and where you park overnight.

Add Your Personal Details

Enter your name, address, date of birth, and occupation.

Declare Your CU80

Select the CU80 conviction code, enter the date of offence, and the 6 points. Declare any other endorsements too.

Compare Your Quotes

Review the quotes from specialist brokers and choose the cover that suits your needs and budget.

What Our Expert Says

One glance. A notification lit up the screen, your hand moved before your brain caught up, and in that fraction of a second everything changed. Six points and a £200 fine for something that lasted less time than reading this sentence.

CU80 is the most common construction and use conviction code issued in the UK. Since 2022, the law covers any interactive use of a handheld device — not just calls or texts, but scrolling, checking a map, even dismissing a notification. For drivers within their first two years, those 6 points trigger automatic licence revocation under the New Drivers Act. You would need to retake both tests from scratch.

The sheer volume of CU80 convictions means specialist brokers have deep experience placing these cases. They know which insurers treat a momentary lapse proportionately rather than applying blanket penalties.

Co-founder of Clean Green Cars

Common CU80 Car Insurance Questions

Related Construction and Use Codes

CU80 sits within the construction and use family of endorsement codes. It is the most commonly issued code in this category.

You may also want to consider temporary car insurance for convicted drivers if you need short-term cover.

Using a vehicle with defective brakes

Compare CU10 quotesCausing or likely to cause danger by reason of use of unsuitable vehicle or parts in dangerous condition

Compare CU20 quotesUsing a vehicle with defective tyre(s)

Compare CU30 quotesUsing a vehicle with defective steering

Compare CU40 quotesCausing or likely to cause danger by reason of load or passengers

Compare CU50 quotesSearch & compare quotes from UK CU80 Car Insurance Providers

Useful Resources

- GOV.UK – Using a Mobile Phone When Driving – The current law on mobile phone use while driving, including what is and is not allowed.

- GOV.UK – Penalty Points and Endorsements – How the penalty points system works, including endorsement codes and expiry dates.

- GOV.UK – View Your Driving Licence – Check your licence online to see your current points and convictions.

- GOV.UK – New Drivers – Rules for new drivers within their first 2 years, including the 6-point revocation threshold.