Why Compare IN10 Car Insurance?

6 To 8 Points Can Push Premiums Up Sharply

IN10 often carries more points than many other motoring offences. Every insurer weights them differently. Clean Green Cars introduces you to specialist brokers who know which brokers who are familiar with insurers that consider IN10 convictions.

Standard Sites May Not Show The Full Picture

Some mainstream insurers may increase your premium or decline to quote after an IN10 conviction. Clean Green Cars introduces you to specialist brokers who consider your individual circumstances and may have access to insurers that assess applications from drivers with IN10 endorsements. Terms, eligibility and premiums vary between insurers.

A Lapse Is Not Always Your Fault

Many IN10 convictions result from administrative errors, direct debit failures, or misunderstandings. Specialist brokers can explain these circumstances to insurers who may take a balanced view.

IN10 Car Insurance At A Glance

- IN10 means using a vehicle uninsured against third party risks under Section 143 of the Road Traffic Act 1988.

- The penalty is 6 to 8 points, a fixed penalty of up to £300 or an unlimited fine at court. Your vehicle may also be seized.

- IN10 is a strict liability offence. It does not matter whether you knew your insurance had lapsed.

- Click the green button above to compare IN10 quotes from specialist brokers.

What Is An IN10 Conviction?

IN10 is a statutory offence under Section 143 of the Road Traffic Act 1988 - using a motor vehicle uninsured against third party risks. Here's how the law defines it:

- Who it applies to - Any person who uses, causes or permits the use of a motor vehicle on a road or public place without at least third party insurance in force. The keeper can be convicted even if they were not driving at the time.

- Why it is strict liability - The prosecution does not need to prove you knew the vehicle was uninsured. The offence is committed the moment the vehicle is used without valid cover, whether your policy was cancelled, lapsed, or never valid for the use in question.

- How it is detected and enforced - Police Automatic Number Plate Recognition (ANPR) flags uninsured vehicles against the Motor Insurance Database (MID) in real time. Officers can seize the vehicle on the spot, and the Motor Insurers' Bureau (MIB) can also take action against uninsured keepers.

| Penalty | Details |

|---|---|

| Penalty Points | 6 to 8 |

| Driving Ban | Discretionary |

| Maximum Fine | Fixed penalty £300 or unlimited fine at court |

| Time on Licence | 4 years on licence from date of offence |

| Spent After | 5 years from date of conviction |

Penalties, endorsement periods and enforcement powers shown here reflect current legislation and guidance at the time of writing. Outcomes vary depending on individual circumstances and court decisions and may change over time. Always check the latest guidance on GOV.UK.

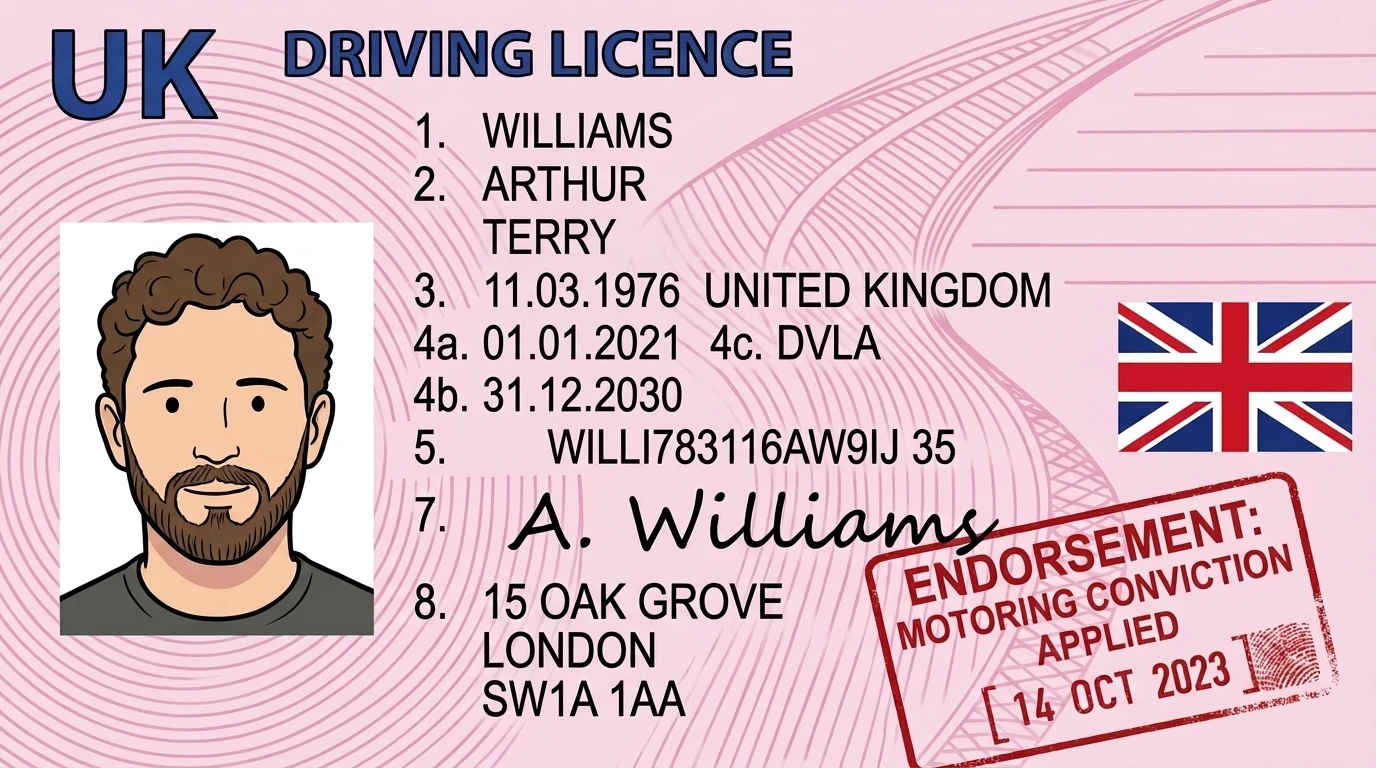

IN10

IN10Can You Get Insurance With An IN10 Conviction?

Typically, yes. IN10 is among the more common conviction codes, and specialist convicted driver brokers may be able to help you compare appropriate cover.

If your vehicle has been seized, car impound insurance could help you get it back.

An IN10 carries 6 to 8 penalty points, and the endorsement stays on your licence for 4 years from the date of the offence. Under the Rehabilitation of Offenders Act 1974, the conviction becomes spent after 5 years. Most insurers ask about the full 5-year period when you apply for cover.

You must declare your IN10 to any insurer while the conviction is active and while they ask about it. Many application forms ask whether you have had any motoring convictions in the last 5 years. If you answer “no” when the conviction is still within that window, your insurer could cancel your policy or decline a future claim.

Specialist brokers who work with convicted drivers know which insurers are more likely to accept IN10 convictions. Clean Green Cars introduces you to these brokers, so you could compare quotes from providers experienced with insurance offences.

Who Needs IN10 Car Insurance?

IN10 is among the more common conviction codes. Here's who typically benefits from comparing IN10 car insurance quotes.

Your Payment Failed Without You Knowing

A direct debit bounced, a card expired, or a bank error left you uninsured without any notification. It was not a choice. Specialist brokers can explain this to insurers who understand that a payment failure is not the same as deliberate evasion.

You Assumed You Were Covered

A paperwork mistake, a misunderstanding about whose policy covered the car, or a renewal that slipped through the cracks. The law does not care about the reason, but specialist brokers do. They can present your circumstances to insurers who can assess the circumstances.

First Offence, Clean Record Otherwise

You had no previous convictions. A single IN10 is your only endorsement and it feels deeply unfair. Specialist brokers know which insurers are likely to treat a single IN10 as a low-risk lapse rather than a pattern of behaviour.

Young Driver Facing Even Higher Costs

You are under 25 and the IN10 has made already-high premiums feel impossible. Six to eight points on a young driver's licence is devastating. Specialist brokers may find options that assess your full profile, not just your age and conviction.

Renewal Has Become Unaffordable

Your current insurer may have applied a significant increase to your premium after the IN10 conviction. Comparing quotes through specialist brokers may help identify insurers that take your individual circumstances into account when assessing your application. Terms, eligibility and premiums vary between insurers.

Worth Knowing: A lapsed direct debit and a deliberate decision not to insure both produce the same IN10 code. Clean Green Cars introduces you to brokers who are familiar with the different circumstances that can lead to an IN10 and may help present your application to insurers that consider individual situations.

What IN10 Car Insurance Covers

An IN10 on your licence does not change what your policy is designed to cover. It changes how much you pay and which insurers will quote you.

Here’s what each level of cover typically may include. Please note that policy features, benefits, terms and conditions vary among insurance providers, so always check the policy wording.

| Feature | Comprehensive | Third Party, Fire & Theft | Third Party Only |

|---|---|---|---|

| Damage to your own vehicle | Yes | No | No |

| Fire and theft protection | Yes | Yes | No |

| Damage to other people's property | Yes | Yes | Yes |

| Injury to other people | Yes | Yes | Yes |

| Windscreen cover | Often included | Rarely | No |

| Courtesy car | Sometimes included | Rarely | No |

Cover Tip: An IN10 conviction does not necessarily limit you to basic cover. In some cases, comprehensive cover may cost less than third party only, depending on your circumstances and the insurer’s assessment. Comparing all three levels of cover through a specialist broker can help identify what options may be available.

What IN10 Car Insurance May Not Cover

One missed detail on your application could mean a declined claim. Here’s what IN10 car insurance usually may not cover.

Standard Exclusions

- Undeclared Convictions - If you do not tell your insurer about your IN10 or any related convictions, they could invalidate your policy and may decline all claims.

- Driving Under the Influence - If you cause an accident while impaired by drink or drugs, your insurer could decline your claim regardless of any other conviction on your record.

- Undeclared Vehicle Use - If your policy covers social use but you are driving for business, your insurer could decline a claim for using the vehicle outside your policy terms.

- Racing or Track Use - Standard policies do not cover racing, track days, or competitive events.

Important Limitations

- Higher Compulsory Excess - Some insurers apply a higher compulsory excess for convicted drivers, which means you pay more before a successful claim is settled.

- Mileage Restrictions - Your policy may limit your annual mileage. Exceeding it could affect whether a claim is paid in full.

- Vehicle Value Cap - Some convicted driver policies may cap the maximum value of vehicle they will insure.

- Named Driver Restrictions - Some policies may limit who else can drive your car after a conviction of this nature.

Extras Worth Adding

Your standard policy is designed to cover the basics. These extras may help fill gaps that could matter after an uninsured driving conviction. Policy claim limits typically apply.

May help cover roadside assistance if your car breaks down away from home, subject to policy limits and conditions.

May help cover your legal costs if you need to dispute fault after an accident, depending on your policy terms.

May help cover the cost of replacing your keys if they are lost or stolen, subject to policy limits and conditions.

May be needed if you have built up years of no claims and want to keep your discount safe after a claim, subject to insurer acceptance criteria.

May pay up to a set amount if you are hurt in a crash and cannot work, depending on your policy terms.

May be needed if you want to prove safe driving habits after your conviction. A black box tracks your speed, braking, and mileage, which could help reduce your renewal price.

What Affects The Cost Of Car Insurance With An IN10 Conviction?

Your quote depends on the number of points, how recently you were convicted, and your overall driving history.

| Key Factor | Impact on Your Price |

|---|---|

| Your IN10 conviction | IN10 carries 6 to 8 points, more than most motoring offences. This could push your premium up considerably. |

| Time since conviction | Your price could drop each year as the IN10 ages. A conviction from several years ago may cost less to insure than a recent one. If you need short-term cover while comparing annual policies, temporary convicted driver insurance could bridge the gap. |

| Other convictions on your licence | An IN10 on top of other motoring convictions could push your price up sharply. |

| No claims discount | A long no claims history could help offset some of your IN10 loading. |

| Your vehicle (group, age, value) | Higher insurance group cars cost more to insure. Choosing a lower group car could help. |

| Annual mileage | Lower mileage usually means lower risk. Make sure your estimate is accurate. |

| Cover level | Comprehensive cover could cost less than third party only for some convicted drivers. Always compare all three levels. |

| Where you live | Your postcode affects your base price before any conviction loading is added. |

Price Insight: IN10 carries 6 to 8 points, more than most motoring offences. But the loading could reduce as the conviction ages, especially if the circumstances behind it were a genuine mistake rather than a deliberate choice.

Ways To Help Manage Your Car Insurance Cost

An IN10 could increase your car insurance premium, but there are steps that could help manage what you pay.

Set Up Payment Safeguards

If a failed direct debit caused your IN10, set up a backup payment method or a calendar reminder 2 weeks before each payment date. Prevention is the best protection against it happening again.

Compare At Every Renewal

Your IN10 loading may reduce over time as the conviction becomes older. It can be helpful to compare quotes at each renewal rather than auto-renewing, to see how insurers are assessing your circumstances. Terms, eligibility and premiums vary between insurers.

Prove Safe Driving With Telematics

A telematics policy provides insurers with information about how you drive. After an IN10 conviction, demonstrating responsible driving behaviour over time may help some insurers assess your risk differently at renewal. The impact varies between insurers and individual circumstances. Terms, eligibility and premiums vary between insurers.

Choose A Lower Insurance Group Car

Cars in lower insurance groups typically cost less to insure, even with an IN10 on your record. If you are changing vehicles, checking the group first could help.

Raise Your Voluntary Excess

Choosing a higher voluntary excess may reduce your premium, depending on the insurer and your circumstances. Make sure the amount is one you could genuinely afford to pay if you needed to make a claim. Terms, eligibility and premiums vary between insurers.

Pay Annually If Possible

Monthly payments often include interest charges. Paying the full year upfront could help reduce what you pay overall.

Add An Experienced Named Driver

Adding someone with a clean licence and years of experience may help some insurers assess your application more favourably, depending on individual circumstances.

Saving Tip: A genuine mistake does not always determine what you pay indefinitely. Compare quotes above - Clean Green Cars introduces you to brokers who understand the difference between a lapsed payment and a deliberate decision.

How To Compare IN10 Car Insurance Quotes

Getting quotes after an IN10 does not take long. Get started above when you are ready.

Enter Your Vehicle Details

Add your registration, make, model, and where you park overnight.

Add Your Personal Details

Enter your name, address, date of birth, and occupation.

Declare Your IN10

Select the IN10 conviction code, enter the date of offence, and the number of points. Declare any other endorsements too.

Complete Your Driving Record

Choose your cover level, add your no claims discount, and confirm any previous claims.

Review Your Quotes

Specialist brokers send you quotes based on your details. Compare prices and cover levels, then pick the one that fits.

What Our Expert Says

Receiving an IN10 can feel alarming, especially when it happened through a genuine mistake. A direct debit failed, a renewal email went to spam, or you assumed the car was covered under someone else's policy. The result is the same: a strict liability conviction for using a vehicle uninsured.

IN10 is recorded under Section 143 of the Road Traffic Act 1988. It does not matter whether you knew your insurance had lapsed - the law does not distinguish between deliberate evasion and an honest error. The penalty is 6 to 8 points, a fixed penalty of up to £300, or an unlimited fine at court. Your vehicle may also be seized.

That sense of injustice is understandable. A lapsed direct debit and a deliberate decision not to insure both produce the same IN10 code. Specialist brokers are familiar with the different circumstances that can lead to an offence and may help present your application to insurers that consider individual situations when assessing risk.

Insurance Expert & Co-founder of Clean Green Cars

Common IN10 Car Insurance Questions

What Is An IN10 Conviction Code?

IN10 is the DVLA endorsement code for using a vehicle uninsured against third party risks under Section 143 of the Road Traffic Act 1988. It carries 6 to 8 penalty points.

How Long Does IN10 Stay On Your Licence?

IN10 stays on your licence for 4 years from the date of the offence. Most insurers ask about convictions for up to 5 years.

Can You Get Car Insurance With An IN10?

Generally, yes. Specialist brokers work with insurers who may consider IN10 applications. Clean Green Cars introduces you to these brokers.

How Many Points Does IN10 Carry?

IN10 carries 6 to 8 penalty points, which is higher than most motoring offences. See GOV.UK penalty points for the full list.

Is IN10 A Strict Liability Offence?

Yes. It does not matter whether you knew your insurance had lapsed. The offence is committed simply by using an uninsured vehicle. The prosecution does not need to prove intent.

Can Your Car Be Seized For IN10?

Yes. Police can seize and crush uninsured vehicles. The Motor Insurers Bureau works with police on enforcement.

What Is The Fine For IN10?

The fixed penalty is up to £300. At court, the fine could be unlimited.

Does A Direct Debit Failure Count As IN10?

Yes. If your payment fails and cover lapses, you could receive an IN10 even if the lapse was completely accidental. The law makes no distinction between accidental and deliberate.

Will IN10 Show On A DBS Check?

IN10 could appear on an enhanced DBS check, particularly for roles that involve driving.

What Happens After I Submit My Details?

After you submit your details, Clean Green Cars introduces you to specialist brokers who handle convicted driver insurance. They contact you directly with quotes. There is no obligation to buy.

Related Conviction Types

IN10 is the main insurance offence code for driving without valid cover. Start with the wider convicted driver insurance hub if you also have points, bans or another endorsement, then compare related offence families below.

Speeding Convictions

SP codes for exceeding speed limits.

Drink Driving

DR codes for alcohol-related offences.

Careless Driving

CD codes for driving without due care.

Search & Compare Quotes From UK IN10 Car Insurance Providers

Useful Resources

- GOV.UK - Vehicle Insurance - Legal requirements for vehicle insurance.

- GOV.UK - Penalty Points - How penalty points work.

- GOV.UK - View Your Licence - Check your points online.

- Motor Insurers Bureau - Information about uninsured driving enforcement.